Multinational enterprises may undertake cross-border restructurings for various commercial reasons. Under the Enterprise Income Tax Law of the PRC and its implementing regulations, resident enterprises are taxable on worldwide income, while non-resident enterprises are generally taxable only on income sourced in the PRC. Accordingly, a cross-border restructuring transaction may give rise to the PRC enterprise income tax ("EIT").

For non-resident enterprises, potential PRC tax exposure may also arise under State Taxation Administration ("STA") Public Notice [2015] No. 7 ("PN 7") in scenarios that indirectly result in the transfer of the PRC equity or assets. (We have discussed the indirect transfer rules under PN 7 in a separate article[1], and therefore do not discuss those issues further here.)

To reduce the tax burden associated with the restructurings, and in line with international tax practice, the PRC tax law provides the Special Tax Treatment ("STT") for corporate reorganizations, under which EIT will be deferred so that no immediate tax liability arises at the time of the restructuring.

In practice, however, the scope for applying the STT in cross-border reorganizations remains highly controversial. Depending on how the relevant rules are interpreted, restructurings that are economically similar but differ in legal form may be treated differently for these purposes. To better explain this issue, we will introduce the applicability of the relevant tax rules, using four typical cross-border restructuring models as case studies, to analyze the potential challenges in implementing the STT for such reorganizations.

01. Basic Rules of the Special Tax Treatment in Cross-Border Restructurings

1.What Is the Special Tax Treatment?

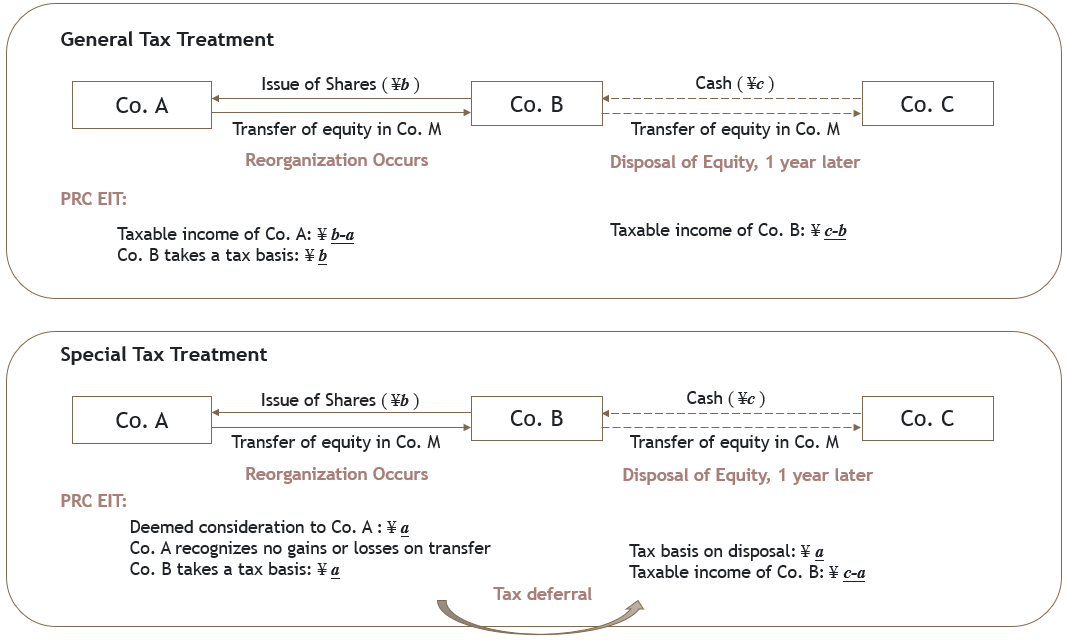

The Notice of the Ministry of Finance and the State Taxation Administration on Several Issues Concerning the Enterprise Income Tax Treatment of Corporate Reorganizations ("Circular 59") provides that qualifying reorganizations may elect the STT. Compared with the general tax treatment, the STT allows for a deferral of tax liabilities at the time of the restructuring transaction by not recognizing gains, while preserving the original tax basis without any step-up.

Example: Company B is a wholly-owned subsidiary of Company A. Company A holds an equity interest in Company M with a tax basis of a yuan. Company B issues shares with a value of b yuan to acquire from Company A the equity interest in Company M. One year later, Company B transfers the acquired equity interest in Company M to Company C for c yuan. Assuming all other conditions for the STT are satisfied, the difference between general tax treatment and the STT in respect of B's acquisition from A is illustrated below:

Figure 1: Comparison of General Tax Treatment and Special Tax Treatment

Accordingly, the STT is not a tax incentive in the sense of a reduction or exemption of tax, because it does not ultimately reduce the overall tax burden. It merely defers the timing of the tax liability and, to some extent, shifts that deferred liability to the party acquiring the restructured assets. This also means that electing the STT will not always produce the optimal tax outcome for a corporate reorganization. For example, in the scenario above, if Company A has accumulated losses, the general tax treatment may be more advantageous. That said, for the general intra-group restructurings without a near-term disposal plan, the STT can avoid the immediate cash-flow pressure from a tax perspective and is therefore often the preferable approach.

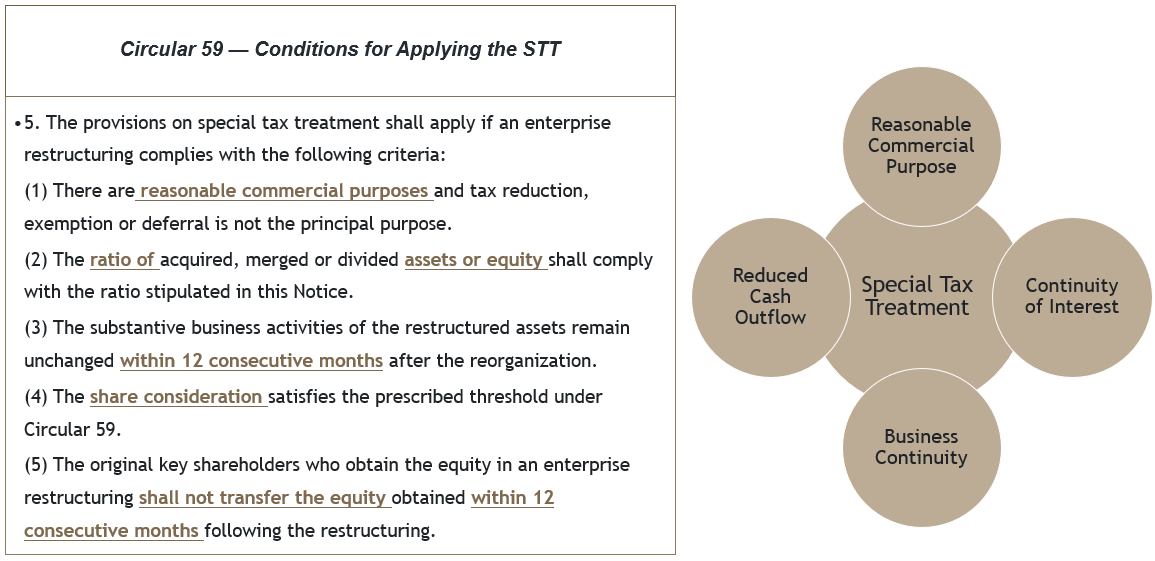

2. Conditions for Applying the Special Tax Treatment

Under Article 5 of Circular 59, a corporate reorganization may qualify for the STT only if all of the following five conditions are satisfied:

Figure 2: Conditions for Applying the Special Tax Treatment to Corporate Restructurings

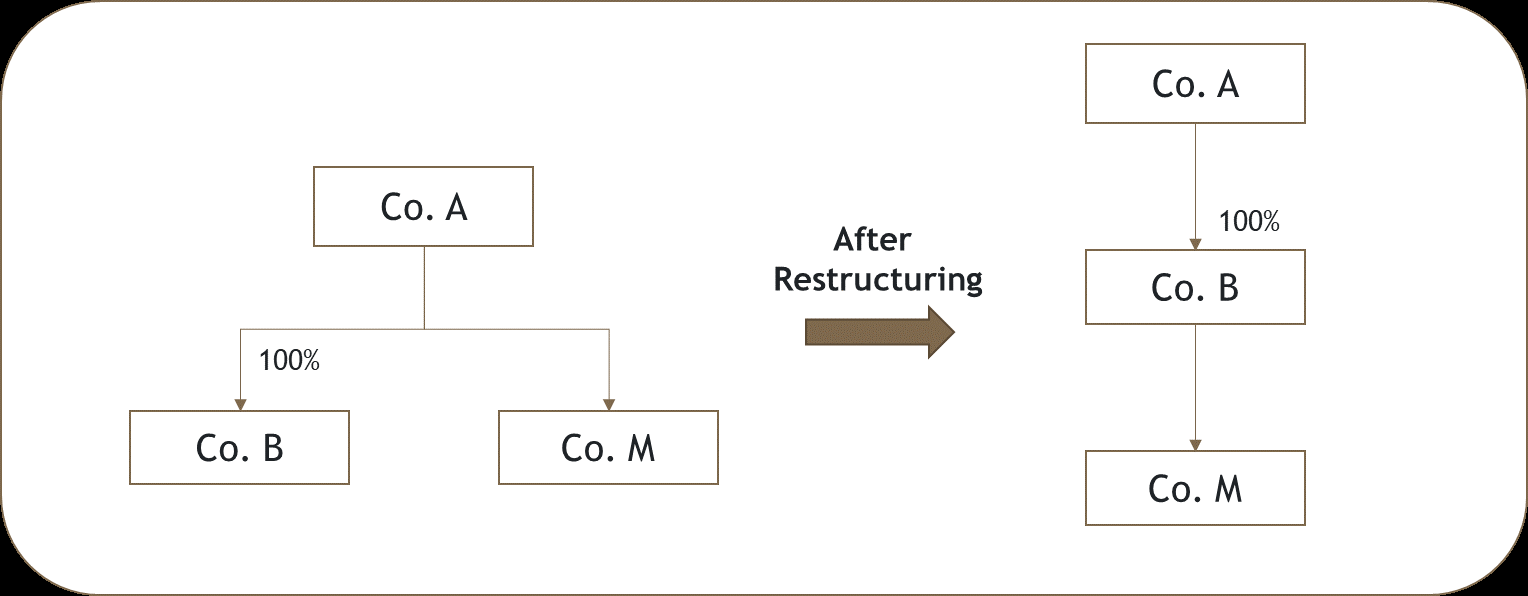

These conditions are the core criteria for determining the eligibility for the STT. They also reflect the theoretical basis of the tax rule: business continuity and the continuity of equity interest. In the example above, once the first-step transaction is completed under the STT, Company A continues to hold an interest in Company M through its shareholding in Company B. Company A's interest in Company M therefore continues.

Figure 3: Continuity of Interest

We understand that the design of Circular 59 reflects not only the theoretical considerations about the fairness of the tax rule, but also an objective of encouraging corporate reorganizations and improving asset utilization.

3. Special Conditions for Applying the Special Tax Treatment in Cross-Border Restructurings

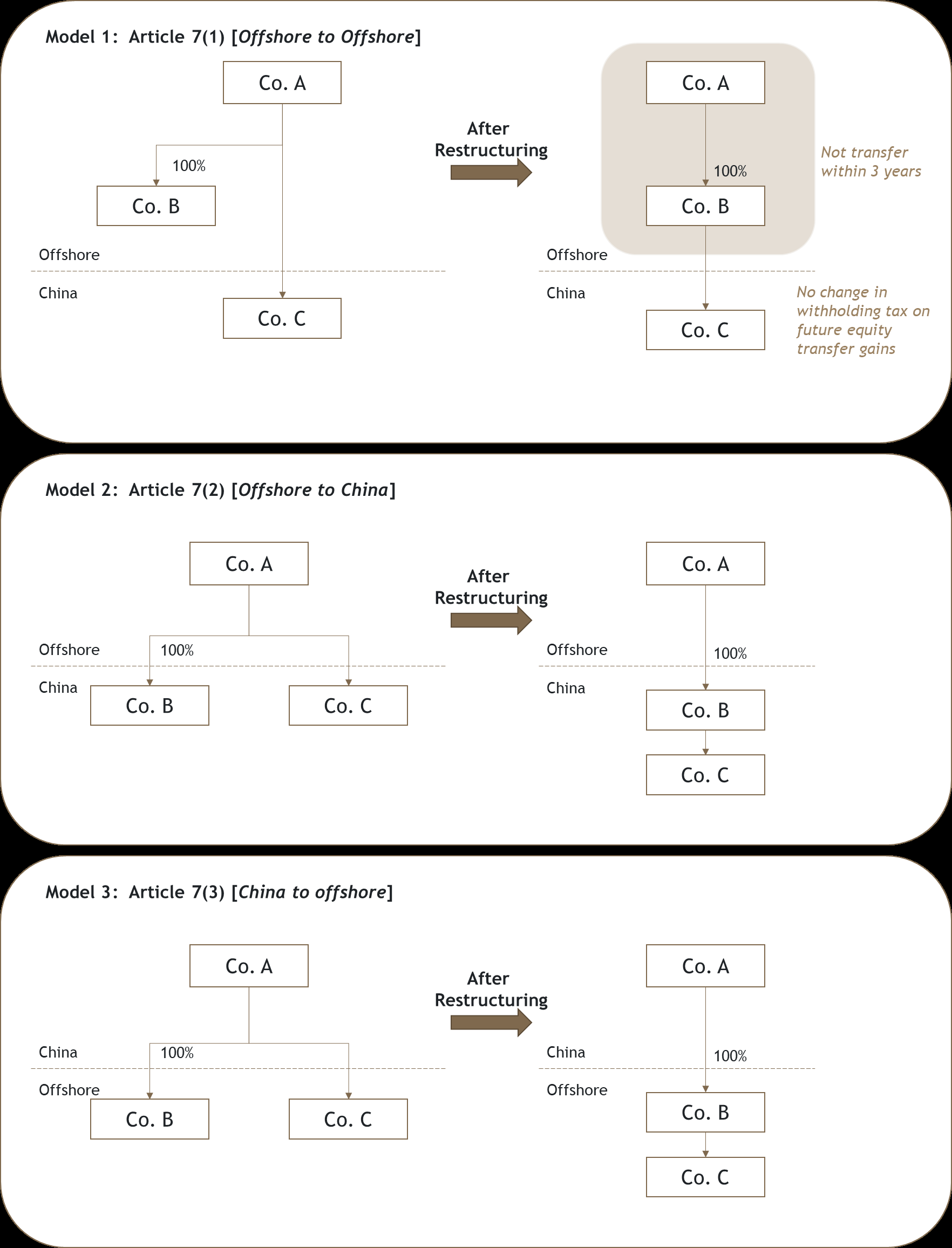

For cross-border reorganizations, in addition to the basic conditions discussed above, Article 7 of Circular 59 requires that one of the following conditions also be satisfied before the STT is applied:

1)A non-resident enterprise transfers its equity in a resident enterprise to another non-resident enterprise that it directly and wholly owns, the transfer does not result in any change to the withholding tax burden on any future gain derived from the transfer of such equity, and the transferor non-resident enterprise gives a written undertaking to the competent tax authority that it will not transfer its equity in the transferee non-resident enterprise within three years;

2)A non-resident enterprise transfers its equity in a resident enterprise to another resident enterprise with which the non-resident enterprise has a 100% direct control relationship;

3)A resident enterprise contributes its assets or equity to a non-resident enterprise that it directly and wholly owns; or

4)Other cases approved by the Ministry of Finance and the STA.

Article 1 of the STA Announcement on Issues Concerning the Application of Special Tax Treatment to Equity Transfers by Non-Resident Enterprises ("Announcement 72") further provides that the circumstances described in Article 7(1) of Circular 59 include transfers of equity in PRC resident enterprises arising from the demerger or merger of overseas enterprises. For example, where one UK company merges with another UK company and that merger results in a change in the shareholding of a PRC investee, the transaction would generally need to be characterized under PRC tax law as an equity transfer, rather than a merger reorganization. Announcement 72 makes clear that such an equity transfer scenario may still fall within Article 7(1).

In summary, the following cross-border reorganization models may qualify for the STT:

Figure 4: Cross-Border Reorganization Models Eligible for Special Tax Treatment

It should also be noted that, although the transaction model described in Model 3 above may qualify for the STT, the applicable treatment is different. The corresponding taxable gain may only be recognized in instalments over a period of up to 10 years, rather than being fully deferred.

As a matter of the tax rules, Article 7 of Circular 59 narrows the range of cross-border transactions eligible for the STT. In our view, the legislative rationale is as follows. In a cross-border reorganization, if restructured assets are transferred from a resident enterprise to a non-resident enterprise, the tax rate applicable on a subsequent disposal of those assets may be reduced, or China may even lose its taxing rights altogether, as in Model 3. If restructured assets are transferred from one non-resident enterprise to another non-resident enterprise, the tax rate applicable on a subsequent disposal may likewise be reduced. For those reasons, the scope of the STT is intentionally confined. In short, to mitigate the administrative difficulty and to safeguard against the erosion of China's tax interests through deferred tax liabilities, the legislation tends to restrict the scope of applying the STT in cross-border reorganizations.

To serve that purpose, the additional conditions emphasize, among other things, a 100% direct control relationship among the relevant parties, thereby limiting the availability of the STT in cross-border cases to certain internal reorganizations.

02. Analysis of the Cross-Border Restructuring Scenarios

In practice, we have seen transaction models that are consistent with the underlying logic of the rules but do not fall squarely within the transaction forms expressly listed. This may give rise to disputes between taxpayers and tax authorities as to whether the STT is available. We illustrate the following four scenarios to assess the application of the STT.

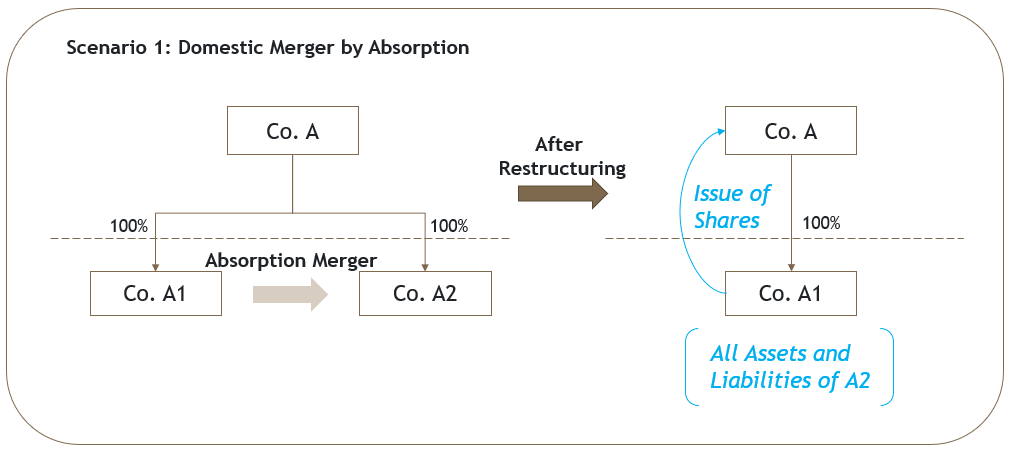

1. Scenario 1: Domestic Merger by Absorption

Background: Overseas Company A (a non-resident enterprise) directly holds 100% of the equity in Domestic Companies A1 and A2 (both resident enterprises). To integrate its domestic operations, A1 absorbs and merges with A2, and issues additional shares to Company A as consideration. The surviving entity A1 does not change the substantive business activities of A2's original assets. In addition, Company A does not transfer the shares it receives within 12 consecutive months after the completion of the restructuring.

Figure 5: Scenario 1 (Domestic Merger by Absorption) Illustration

This scenario involves: (1) A2 transferring all of its assets and liabilities to A1; and (2) A1 issuing its own shares to A2's shareholder, Company A, as the consideration. However, the restructuring does not fall within the transaction types specified in Article 7 of Circular 59.

Article 7 of Circular 59 provides that, where an enterprise undertakes an equity acquisition or asset acquisition transaction involving parties inside and outside China, the transaction may qualify for the STT only if, in addition to satisfying Article 5, such transaction also meets the additional conditions set out in Article 7. Based on our observations in practice, there are several views on the scope of Article 7:

a)Apart from the expressly listed equity acquisitions and asset acquisitions, no other types of cross-border reorganizations - including mergers and demergers - may qualify for the STT.

b)Other forms of cross-border reorganization, apart from equity acquisitions and asset acquisitions, are not subject to the restrictions in Article 7 and may qualify for the STT so long as they satisfy Articles 5 and 6, without the need to meet any further requirements.

c)Because Announcement 72 expressly extends Article 7(1) to mergers and demergers, but contains no similar extension for Article 7(2) or 7(3), it implicitly excludes the possibility of applying the STT to Scenario 1 above.

d)Announcement 72 demonstrates the need to bring mergers and demergers within the scope of Article 7. In a specific transaction, the question should be analyzed on the basis of substance over form to determine whether such transaction falls within Article 7 of Circular 59.

In our view, first, on a textual reading of Article 7, and having regard to its role and character within the overall structure of Circular 59, it is more reasonable to treat mergers and demergers as falling within the scope of consideration. Second, even if cross-border mergers and demergers are regarded as being subject to the additional conditions in Article 7, in certain merger or demerger scenarios - including the present scenario - Company A's 100% controlling interest in the merged assets and liabilities never changes. Moreover, if Company A later transfers its shares in A1, or A1 transfers the merged assets, the applicable tax rate would not decrease and could even increase. Because of the special nature of mergers and demergers, the policy objectives served by the restrictions in Article 7 are therefore substantially achieved. On that basis, we tend to believe that Scenario 1 also presents a reasonable basis for applying the STT.

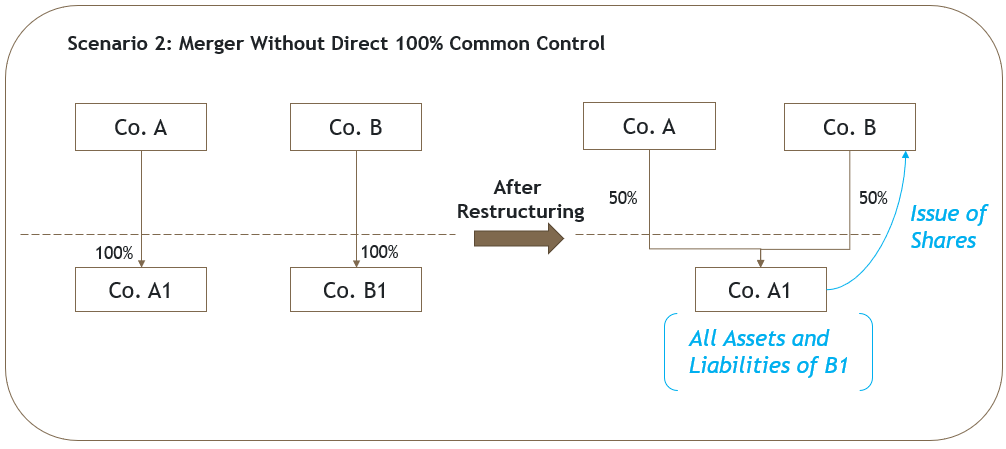

2. Scenario 2: Merger Without Direct 100% Common Control

Background: Overseas Companies A and B (both non-resident enterprises) each hold 100% of the equity in Domestic Companies A1 and B1, respectively. Companies A and B are members of the same multinational group. To integrate the group's resources in China, the group decides that A1 will absorb and merge with B1. The original shareholders, Companies A and B, will hold equity interests in the surviving entity, A1, in proportion to the relative fair market values of A1 and B1 before the merger, with each holding a 50% interest in this example. Post-merger A1 does not change the substantive business activities of the restructured assets. In addition, Company B does not transfer the shares it receives within 12 consecutive months after the completion of the restructuring.

Figure 6: Scenario 2 (Merger Without Direct 100% Common Control) Illustration

Scenario 2 is similar to Scenario 1 in that it may face ineligibility because of interpretive issues concerning the types of reorganization to which the STT for cross-border reorganizations applies. What makes Scenario 2 more complex is that the merging parties and their shareholders do not satisfy the requirement of a 100% direct control relationship, and thus appear to depart even further from the conditions in Article 7 of Circular 59. From a substantive perspective, however, if Companies A and B are ultimately 100% controlled by the same ultimate controller, then, on a look-through basis, the continuity of controlling interest is essentially the same as in Scenario 1. If Scenario 1 presents a reasonable basis for the STT, there is also reasonable to consider whether the interpretation and application of the relevant rules may also be extended to Scenario 2. In our view, that possibility should not be fully ruled out.

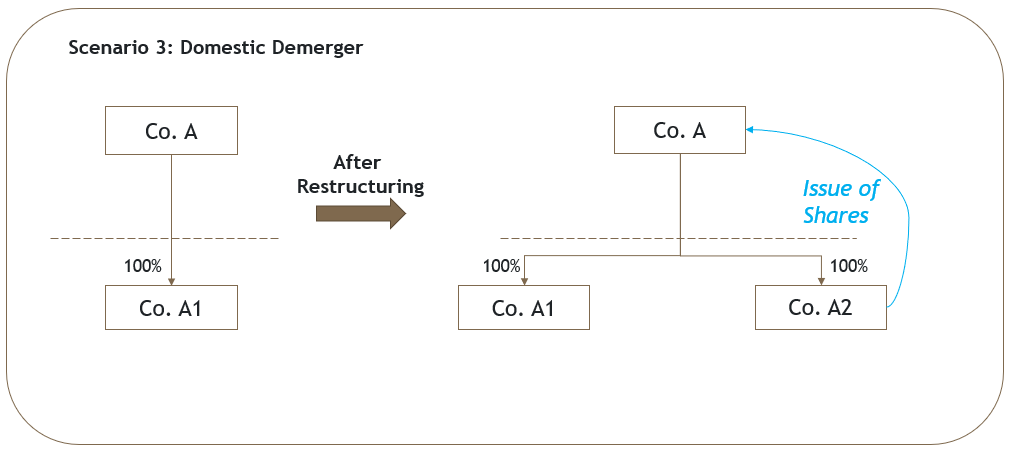

3. Scenario 3: Domestic Demerger

Background: Overseas Company A (a non-resident enterprise) holds 100% of the equity in Domestic Company A1. To separate domestic business lines, A1 is demerged into Companies A1 and A2. Neither A1 nor A2 changes the substantive business activities of the original assets. In addition, Company A does not transfer its equity in A2 within 12 consecutive months after the completion of the restructuring.

Figure 7: Scenario 3 (Domestic Demerger) Illustration

This scenario involves: (1) A2 acquiring the assets and liabilities of the part of A1’s business; and (2) A1's shareholder, Company A, receiving equity in A2 as the consideration.

Clearly, Scenario 3 is not one of the demerger transaction types expressly covered by Announcement 72 as falling within Article 7 of Circular 59. Accordingly, as with the preceding scenarios, the application of the STT to Scenario 3 would require the interpretive issue regarding the scope of cross-border reorganization types to be resolved.

Consistent with our analysis of Scenario 1 and 2, this scenario may likewise substantially satisfy the policy objectives served by the restrictions in Article 7 when viewed from the perspective of transaction substance and legislative purpose. The demerger does not change Company A's 100% controlling interest in the overall domestic assets, and a future transfer of the post-demerger equity would not result in a different withholding tax burden as compared with the current structure. Accordingly, on the interpretive approach to Article 7 discussed above, we tend to consider that Scenario 3 also presents a reasonable basis for applying the STT.

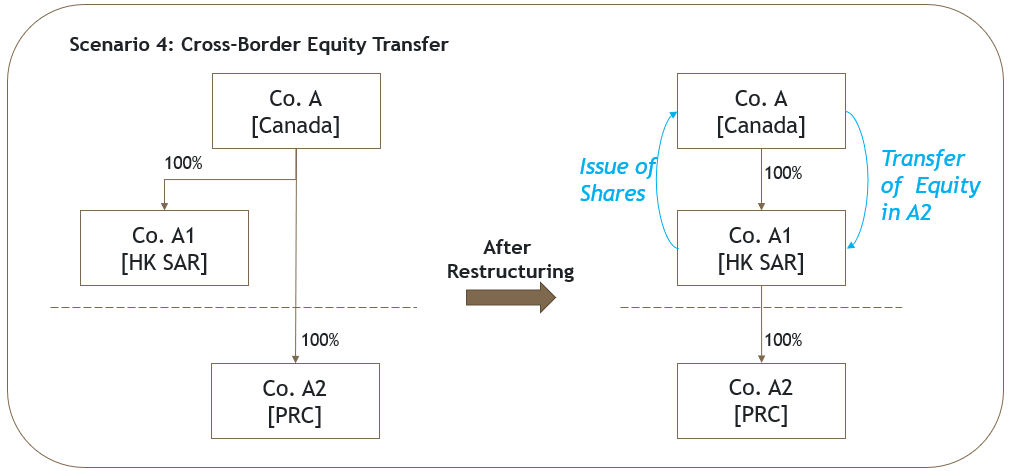

4. Scenario 4: Cross-Border Equity Transfer

Background: Canadian Company A (a non-resident enterprise) holds 100% of the equity in Hong Kong Company A1 and 100% of the equity in Domestic Company A2. To enable A1 to act as regional headquarters, Canadian Company A transfers its 100% equity interest in A2 to Hong Kong Company A1, and A1 issues shares to Company A as the consideration for the acquisition of the A2 equity. Canadian Company A undertakes not to transfer its equity in Hong Kong Company A1 within three years.

Figure 8: Scenario 4 (Cross-Border Equity Transfer) Illustration

In terms of transaction form, this scenario falls within Article 7(1) of Circular 59: a non-resident enterprise (Company A) transfers equity in a PRC resident enterprise (Company A2) to another non-resident enterprise (Company A1) that it directly and wholly owns. The withholding tax burden on any future gain from the transfer of that equity would not change, and Canadian Company A undertakes not to transfer its equity in Hong Kong Company A1 within three years.

In practice, however, we have seen tax authorities raise the following questions in relation to the application of the STT in this scenario:

1)Question 1: Would a change in the dividend withholding tax rate constitute a basis for denying the STT? Assume that Company A and Company A1 are tax residents of Canada and Hong Kong SAR, respectively, and that each satisfies the beneficial ownership requirement. Once A2's shareholder changes from Canadian Company A to Hong Kong Company A1, dividends paid by A2 to Hong Kong Company A1 in the future would be subject to the preferential 5% under the Chinese mainland-Hong Kong tax arrangement, rather than the 10% under the PRC-Canada tax treaty. Should that be taken into account as a reason to deny the STT in this cross-border reorganization?

As a matter of the rules, Article 7(1) expressly focuses on changes in the withholding tax burden on gains from the transfer of the equity; it does not address dividend withholding tax. However, as a general condition for the STT, if the principal reason for Scenario 4 is to avoid a higher rate of tax on dividend distributions, the transaction may be vulnerable to challenge under the reasonable commercial purpose requirement. Whether that concern arises will depend on the specific commercial purposes of the transaction in the particular case.

2)Question 2: If Company A1 transfers the equity in A2 after 12 months, should the STT cease to apply and the tax then be collected under the general tax treatment?

As a matter of the rules, Article 7(1) requires only that the transferor, Canadian Company A, does not transfer its equity in the transferee, Hong Kong Company A1, within three years. It does not impose any additional restriction on A1's transfer of A2's equity. Whether A1 may transfer the equity in A2 should therefore be determined only by reference to the general condition in Article 5 that the substantive business activities of the restructured assets remain unchanged for 12 consecutive months after the reorganization. A contrary view might argue that the additional condition in Article 7(1) should be read holistically, such that the continuity of Company A's 100% controlling interest must be maintained for three years.

3)Question 3: Further financing arrangements may follow the completion of this transaction. For example, if Company A1 accepts capital contributions from new investors within three years, thereby diluting Company A's shareholding in A1, should the STT cease to apply and the tax then be collected under general tax treatment?

The essence of this issue is whether dilution of a shareholding caused by a capital increase constitutes a transfer of the consideration shares. This issue is not unique to the STT in cross-border reorganizations; it is also a common point of dispute in domestic corporate reorganizations.

In our view, from the perspective of legal relationships, a capital increase and an equity transfer differ significantly in terms of the relevant parties and the specific rights and obligations involved. From an economic perspective, if the capital increase itself has a reasonable commercial purpose, dilution of the original shareholder's percentage interest is not economically equivalent to a transfer of the equity interest. That said, in practice, this issue remains prone to dispute because of various anti-avoidance concerns.

03. Practical Risks and Our Suggestions

While the STT rules facilitate M&A reorganizations, they also create challenges for cross-border restructurings. Circular 59 restricts the range of cross-border transaction forms eligible for the STT, which may exclude many common transaction models. In our view, whether the STT can apply to a particular cross-border reorganization still requires a careful analysis of the transaction's economic substance and an assessment against the substantive requirements of the rules.

Procedurally, under the current regulatory framework, a taxpayer seeking the STT must submit a complete filing package. In practice, because of the complexity of the intended transactions and the vagueness of the tax rules, the filing process often requires substantive communication with the competent tax authority. This is particularly true where a merger involves tax deregistration, in which case the tax authority's review may be more involved.

Within the current prudent tax enforcement climate, Chinese tax authorities tend to interpret Circular 59 cautiously for cross-border restructurings. Consequently, any transaction structure not explicitly addressed by the rules - regardless of its substantive compliance with the Circular 59's intent - faces a significant practical barrier to obtaining the STT.

From the perspective of tax certainty, we believe that advance communication is highly valuable in complex cross-border restructurings. For taxpayers in Shanghai, Beijing, Shenzhen and a few other major cities, it may also be worth making use of the advance ruling regime[2], to achieve certainty. If you would like to discuss the application of the STT in cross-border reorganizations, please contact us.

*"Hong Kong" or "Hong Kong SAR" means the "Hong Kong Special Administrative Region of the People's Republic of China".

Footnotes:

[1] see Guide to Taxation of Offshore Indirect Transfers in China

[2] see Shanghai Pilots Advance Tax Ruling System

Source: King & Wood Mallesons

Authors:

Yu Yue (Jessie), Partner, Regulatory & Compliance Group, jessie.yu@cn.kingandwood.com; Areas of Practice:tax advisory, tax disputes resolution, transfer pricing and private wealth management

Thanks to interns Shen Lin and Wang Zhenyu for their contributions to this article.